It’s usually in the Mid-Session Reviewwhich comes out in July. But no table of forecasts is included this year (you can check–I did!). Which begs the question — how did they estimate the revenues going forward if they didn’t have GDP projections?

Now, one could argue that the Administration couldn’t make a forecast given uncertainty regarding the OBBB’s passage and contents (the forecast is usually nailed down a couple months in advance, and OBBB was signed into law on July 4). Nonetheless, internally, they needed something in order to calculate a difference under administration preferred policies. I doubt they did what Vought did 2020 — just retained unchanged the January 2020 forecast associated with the FY2021 budget request in the July Mid-Session Review (see discussion here).

So, here’s CEA’s assessment of the OBBB summarized:

Source: CEA, The One Big Beautiful Bill – Legislation for Historic Prosperity and Deficit Reduction (June 2025).

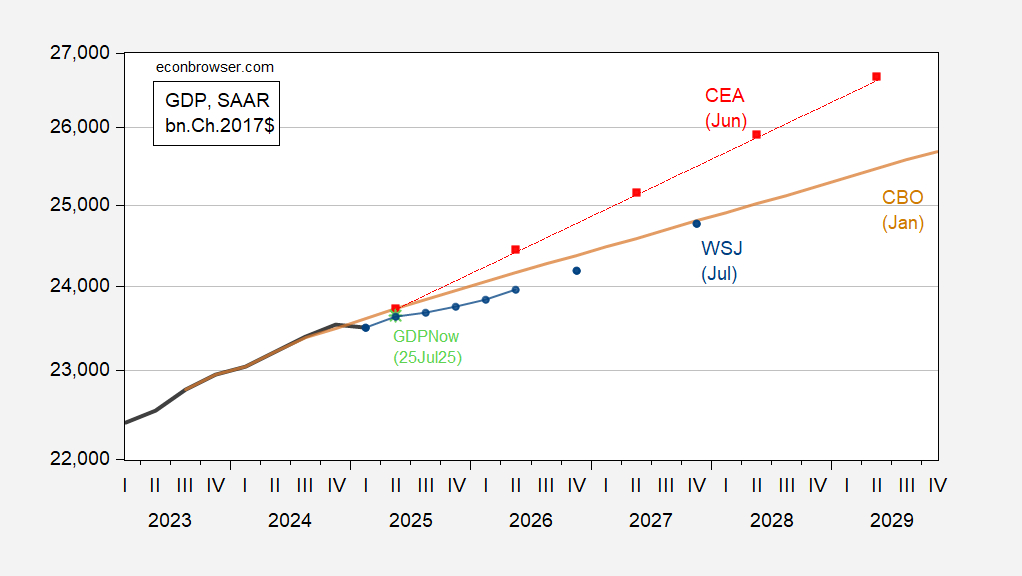

How did CEA estimate this effect?

Source: CEA, The One Big Beautiful Bill – Legislation for Historic Prosperity and Deficit Reduction (June 2025)P10.

Here’s the CEA’s forecast illustrated (I have used the midpoint of the 4.6%-4.9% level impact from the Table).

Figure 1: GDP (bold black), CBO current law projection of January (tan), implied CEA forecast using CBO current law (red squares), mean forecast from July WSJ survey (blue circles), GDPNow of 7/24 (light green *), all in bn.Ch.2017$ SAAR. Source: BEA 2025Q1 3rd release, CBO January 2025, CEA (2025)WSJ survey, Atlanta Fed, and author’s calculations.

So if you thought the (dynamic scoring) revenue projections for the OBBB from CEA were fantastical (per CRFB), you would have to agree that the growth projections are similarly fantastical.

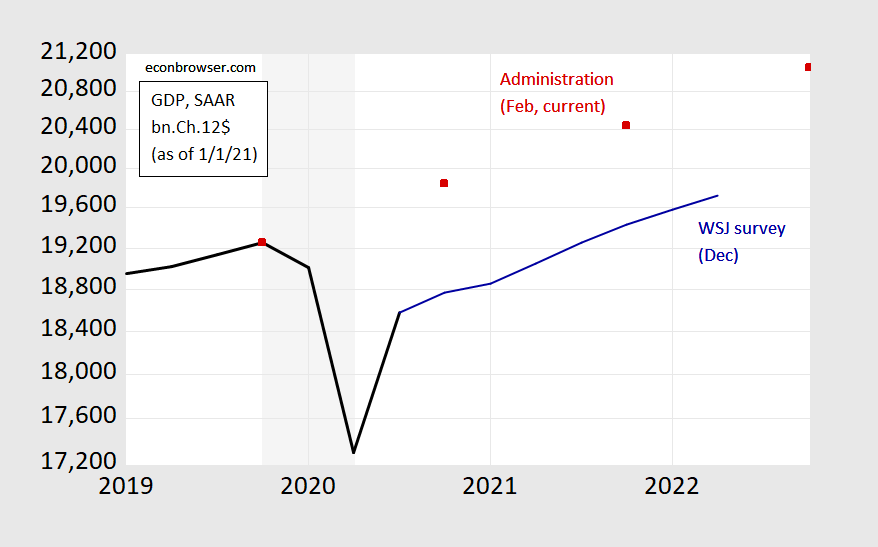

As noted above, this is not the first time the Trump administration has sought to hide their views on the economy’s likely path. Back in 2020, the Administration kept the same forecast in the Mid-Session Review as had been forwarded in February in the FY2021 budget, so that the pandemic was essentially ignored. Here’s my retrospective from the beginning of 2021.

Figure 2: GDP as reported (black), Administration current forecast (red squares), and WSJ December 2020 survey mean (blue). Trough assumed to be 2020Q2. Source: BEA, OMBWSJ, NBER, and author’s calculations.

So…don’t believe anything that’s coming out of this administration economics-wise. And, I am sad to say, that includes CEA (see other written material here), aside the purely data product of Economic Indicators (CEA-Jean joint).