Allies of President Donald Trump are promoting a new type of tax-favored savings account that bears his name as a way for families to build savings over the long term.

Under the rules, babies born between Jan. 1, 2025, and Dec. 31, 2028, will receive $1,000 in seed money from the federal government to launch the account. Parents could make additional deposits but aren’t required to.

Trump’s allies say the accounts are a way for American families to accumulate savings over the long term.

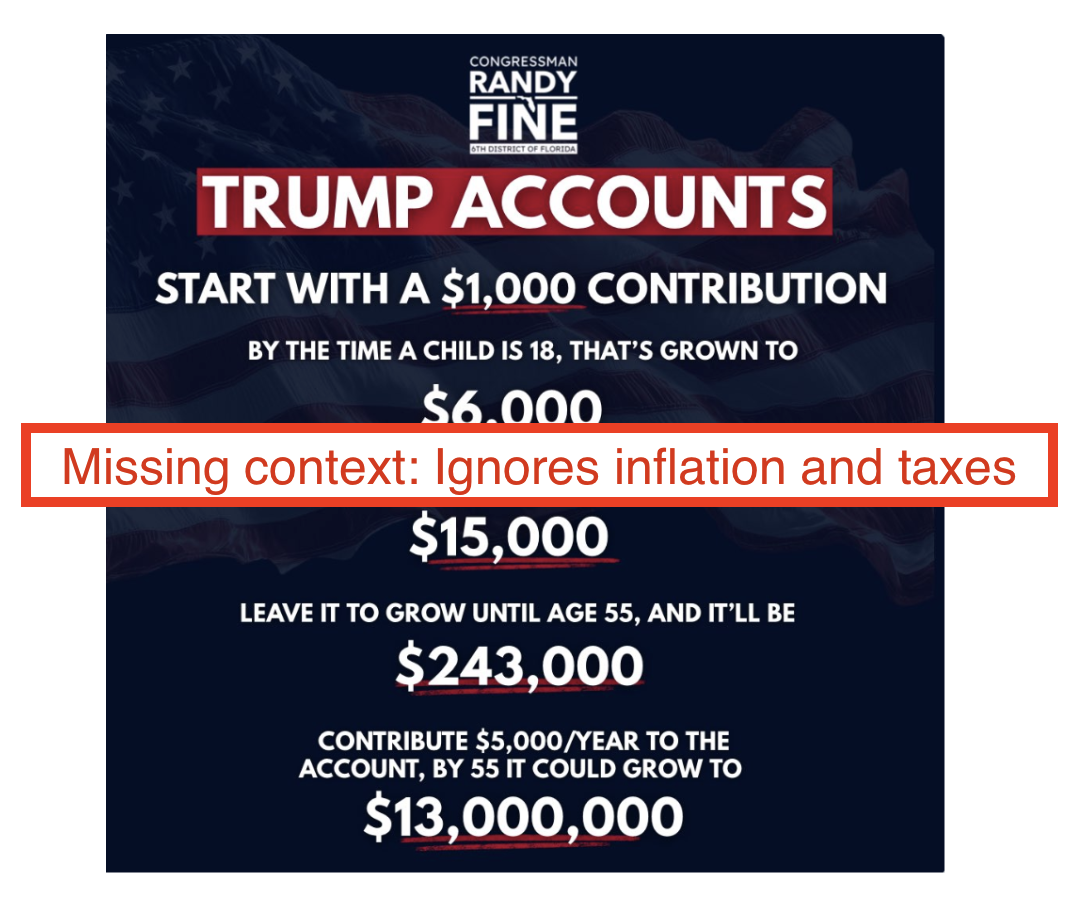

In a Jan. 29 X postU.S. Rep. Randy Fine, R-Fla., said that even with no additional deposits, a $1,000 account would grow to $6,000 by the time the child is 18; to $15,000 by age 27; and to $243,000 by age 55. (The White House shared similar figures.)

(Screengrab from X)

Mathematically, the numbers Fine cited are in the ballpark — but they ignore important context. The estimate doesn’t factor in inflation, the risk of lower investment returns in the future, and the taxes upon withdrawal.

Those factors would substantially reduce Fine’s $243,000 figure, personal finance experts say. An analysis by Alan D. Viard, an emeritus senior fellow at the conservative American Enterprise Institute, found projections like Fine’s “grossly exaggerated.”

Vickie L Bajtelsmit, an emerita professor of finance and real estate at Colorado State University, said, “As usual, politicians like to provide the most optimistic outcomes without any of the caveats.”

Fine’s office did not respond to an inquiry for this article.

What are Trump accounts?

Trump first proposed these accounts as a 2024 presidential candidate; their enactment earned him a Promise Kept in our MAGA-Meter.

Starting July 4, parents will be able to open a Trump account for any child under 18 who has a Social Security number. Parents can deposit up to $5,000 a year into a fund that tracks the growth of the overall stock market. The $5,000 annual cap will eventually be indexed for inflation.

Employers can also deposit up to $2,500 per year (which counts against the $5,000 annual limit). The employer’s contribution would not count toward the employee’s taxable income.

Generally, the child cannot withdraw the funds before turning 18 without paying a 10% penalty plus taxes. Once they turn 18, the Trump accounts would be treated like a traditional Individual Retirement Accountwith withdrawals taxed until the account holder is six months shy of 60 years old. However, withdrawals for education and home purchases get a break; they are subject to tax but not a penalty.

The Trump account has attracted the most attention for one feature: a $1,000 starter deposit from the federal government for qualifying babies.

An investment calculator maintained by the federal Securities and Exchange Commission shows that using an average annual investment gain of 10%, $1,000 would grow to almost $245,000 over 55 years, in line with the amount in Fine’s post.

Many account holders will likely withdraw their funds penalty-free for higher education or home purchases. This means the accounts would only accumulate investment gains for between 18 and 30 years, not 55, Bajtelsmit said.

Future stock market gains may not match the historical average

The historical annual average gain for the U.S. stock market is about 10%. But “most experts think that the average moving forward will be less than the historical average,” Bajtelsmit said.

Analysts say the stock market’s price is currently elevated by historical standards, making it harder for future gains to be as robust as past gains. Six major investment firms’ forecasts of annual U.S. stock returns over the next decade range from 3.1% to 6.7%, according to Morningstaran investment research company, and projected returns over the next 30 years range from 4% to 7%.

At a 6.7% annual average return, $1,000 would grow to about $40,000 over 55 years.

Management fees also could eat into the average annual return.

What impact could inflation have?

The $243,000 figure sounds appealing, but what would its purchasing power be in 2081? Quite a bit less than that, experts say. “Regardless of what rate of return you assume, it will buy less than you think,” Bajtelsmit said.

Even a modest 2% inflation rate would take a big bite. An inflation-adjusted investment gain of 8% — a 10% investment gain minus 2% inflation — would produce about $81,000 after 55 years, or about one-third of the amount Fine cited.

However, “2% inflation for the next 55 years may be an overly optimistic guesstimate of future inflation,” Brookings Institution economist Gary Burtless said.

Combining 10% investment returns with 3% inflation would produce just under $47,000 over 55 years.

What could the tax bite be?

After accounting for inflation and returns potentially below 10%, the amount in the account would decline further upon withdrawal because of taxes.

Using less favorable assumptions — a 6.7% annual average return (rather than 10%) and 3% inflation — the initial $1,000 would be worth about $7,651 in today’s dollars in 55 years. Then, at withdrawal, a typical accountholder could be hit by at least a 12% federal income tax and a 4% state income tax, cutting their take to $6,427 — just 2.6% of the amount Fine’s post cites. (Some states, like Fine’s home state of Florida, don’t have an income tax; this calculation will vary depending on the accountholder’s state of residence.)

Experts say these caveats don’t necessarily undermine the idea behind Trump accounts — particularly the initial $1,000 in free money.

“The people who will benefit the most from this are those who might not otherwise have access or the ability to save a lot,” Bajtelsmit said. “The problem is the exaggeration of returns.”