Today we are fortunate to be able to present a guest contribution written by Rashad Ahmed (Andersen Institute for Finance and Economics). The views presented are solely those of the author. A version of this article was posted at ARC blog.

In less than a month, global oil prices surged past $100 per barrel following U.S. and Israeli strikes against Iran. West Texas Intermediate (WTI), the North American crude benchmark, rose from around $65 and peaked around $116, while Brent, the global benchmark used to price most crude grades, climbed from about $70 to $118. The key question now is whether high oil prices persist and materially raise the risk of a U.S. recession.

Historically, the macroeconomic consequences of oil shocks have depended less on oil prices than on the source and persistence of the shock, the policy response, and the economic conditions into which they arrive. By that standard, today’s economy looks very different from the one that confronted the oil crises of the 1970s.

The U.S. economy’s dependence on oil has declined substantially over the past half century. Energy expenditures as a share of GDP have fallen by more than half since the 1970s, reflecting productivity gains and the growing dominance of services. The shale boom has transformed the United States from a major net importer into one of the world’s largest oil producerspartially offsetting the domestic impact of higher prices. Meanwhile, deep and liquid derivatives markets allow firms to hedge energy price volatility more effectively than in earlier decades.

Even so, oil shocks can weigh heavily on a cooling economy that has already faced a series of supply shocks. To assess current risks, it is useful to first examine the economic backdrop and then consider what markets are signaling.

The Economic Backdrop

The labor market entered 2026 with limited momentum. Hiring remained subdued, with little change in payrolls for the year as firms grew more cautious amid tariff uncertainty and rising geopolitical tensions. For energy-intensive sectors including airlines, agriculture, manufacturing, and transportation, the surge in oil prices adds further pressure through higher input costs.

Inflation, meanwhile, was already above the Federal Reserve’s 2 percent target before the conflict began. Prices rose 2.8 percent over the year ending in January, while core inflation excluding food and energy increased 3 percent. A sharp rise in oil prices is unambiguously inflationary, raising costs for both firms and households. The effects appear through higher prices for refined products such as gasoline, diesel, and jet fuel, as well as oil-intensive materials like plastics and fertilizers. Markets have responded accordingly: one-year U.S. inflation swaps have risen to 3.2 percent, up 70 basis points from 2.5 percent on February 27.

Households also entered the year with moderate real income momentum. Higher energy prices could further erode real disposable income by reducing purchasing power and shifting spending toward fuel and utilities and away from other goods and services, creating broader demand headwinds. If elevated oil prices persist, what begins as an inflationary impulse could ultimately give way to demand destruction and disinflation. These pressures can propagate across consumer-facing sectors, spreading the effects of higher oil prices throughout the economy. The resulting drag on consumers can also weigh on equity markets and investor sentiment, reinforcing broader economic weakness.

The Message from Markets

Forward-looking market indicators suggest recession risk has risen meaningfully since the conflict began.

Prediction markets now assign substantially higher odds of a downturn. On Kalshithe probability of a U.S. recession in 2026 almost doubled from about 20 percent to 39 percent, with similar movements observed on Polymarket. Institutional forecasters have also revised their recession probabilities upward. Goldman Sachs raised its 12-month recession probability to 25 percent, citing rising oil prices alongside a weakening labor market, while Moody’s places recession odds above 50 percent following the oil price surge. Economists surveyed by the Wall Street Journal put the probability of a recession at 32 percent, up from 27 percent the previous month.

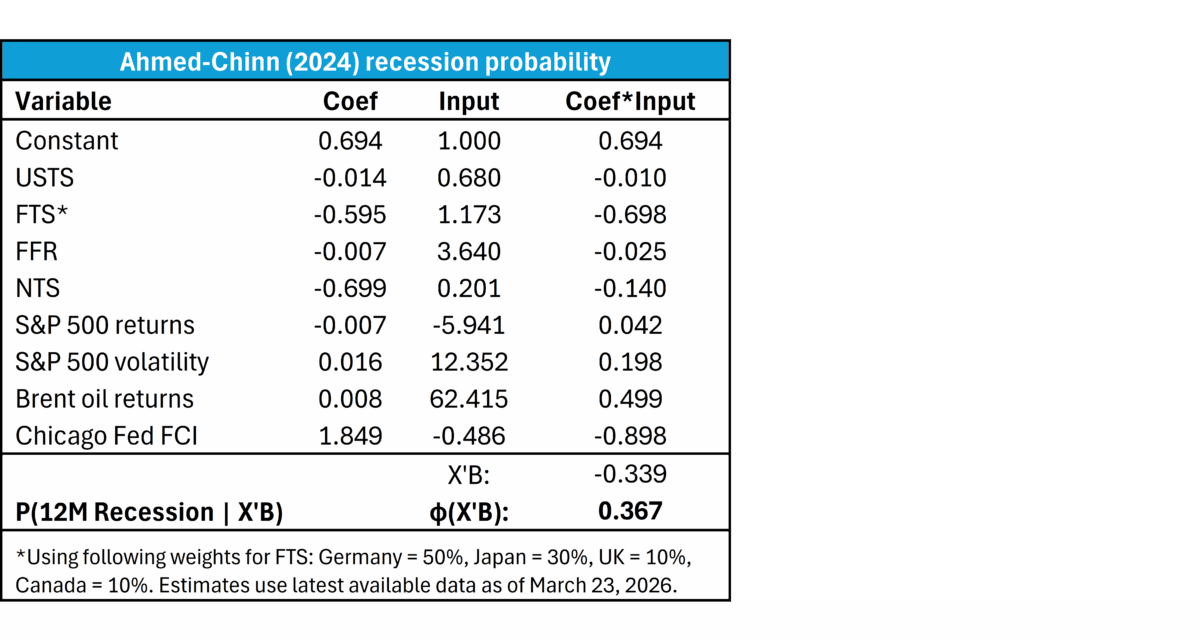

Oil prices, however, are only one component of the broader macro outlook. In Ahmed and Chinn (2024)we develop a recession-probability model based on market indicators including oil prices, U.S. and foreign yield curves, equity market returns and volatility, and broad financial conditions.[1] Updating the model with current data, including a 62 percent rise in oil prices over the past three months, produces a 12-month recession probability of 36 percent, closely aligned with prediction markets and survey forecasts, and between the Goldman Sachs and Moody’s estimates.

A counterfactual exercise highlights the importance of the oil shock. The model-implied recession probability drops to 19.7 percent if we assume no change in oil prices, suggesting the recent price surge has had an economically meaningful effect on recession risk.

Still, several traditional recession indicators remain relatively stable. The U.S. yield curve is not inverted. Foreign yield curves, such as those of Germany, Japan, the United Kingdom, and Canada, also remain steep. The S&P 500 index is currently down about 8.5 percent from its highs, roughly half the magnitude of last year’s largest drawdown and only one-third of the 2022 bear market. Credit spreads have widened as well, albeit modestly so far. Even so, financial conditions could deteriorate quickly if the conflict continues to escalate.

The Fed’s Response

Historically, oil shocks preceded several, but not all, U.S. recessions (Figure 1). Even geopolitical oil shocks (shaded in red) did not uniformly lead to recessions.[2] The historical record instead underscores three points: the economic effects of oil shocks are not mechanical, the shock persistence matters, and monetary policy responses that play a central role.

The geopolitical oil shocks of 1973 (Yom Kippur War), 1979 (Iran Revolution and Iran-Iraq War), and 1990 (Gulf War) were followed by recessions. In each episode, oil prices rose sharply and remained elevated for at least a year, inflation accelerated, and the Federal Reserve tightened policy aggressively.

By contrast, oil shocks associated with the 2003 Iraq War and 2011 Arab Spring and Libyan civil war were not followed by recessions, and monetary policy did not tighten materially. The 2022 oil shock following Russia’s invasion of Ukraine coincided with significant Fed tightening to contain pandemic-era inflation. Even so, the economy ultimately avoided a recession, supported in part by the residual effects of aggressive fiscal stimulus implemented during the 2020 pandemic.

Current policy expectations remain cautious. The Federal Reserve’s latest projections do not incorporate a sharp rise in inflation or policy rates. And while futures markets have priced out the rate cuts expected earlier in the year, they anticipate little change in policy rates by year-end. But with inflation risks and recession risks pulling policy in opposite directions, the outlook for interest rates remains unusually uncertain. Market expectations of unchanged policy rates may therefore be underpricing the likelihood of a large directional move.

Whether a downturn ultimately materializes will depend on the persistence of elevated oil prices, the Federal Reserve’s policy response, and whether repeated supply shocks reinforce inflation dynamics. Sustained upside risks to inflation could prompt more preemptive monetary tightening as policymakers seek to keep inflation expectations anchored.

At the same time, events in Iran continue to evolve rapidly. In an adverse scenario – one in which the conflict extends and escalates dramatically – demand destruction could intensify and financial conditions could deteriorate sharply. Under such circumstances, recession risks would rise materially, potentially shifting the Federal Reserve’s priority from containing inflation to supporting the economy through interest rate cuts.

[1] NBER working paper version can be found here: https://www.nber.org/papers/w30737.

[2] The seven red shaded geopolitical oil shocks include: the Yom Kippur War (1973), the Iranian Revolution and Iran-Iraq war (1979), the Gulf War (1990), the Iraq War (2003), the Arab Spring and Libyan Civil War (2011), the Russia-Ukraine War (2022), and the current US/Israel-Iran conflict (2026).